When will you retire? How to check when you could afford to stop work

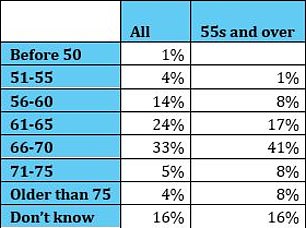

A third of adults across all age groups anticipate retiring between ages 66 and 70, new research reveals.

Just 5 per cent expect to stop work before they are 55, while 14 per cent reckon they could manage it by 56-60 and 24 per cent are targeting 61-65.

Almost a fifth think that they will retire before the age of 60.

But many people are unable or unwilling to set a date, with 16 per saying they don't know in a poll by Hargreaves Lansdown.

The state pension age is currently 66 and will gradually rise to 67 between 2026 and 2028. Meanwhile, the minimum age to draw on a private pension will rise from 55 to 57 overnight on 6 April 2028.

People in their mid to late 40s and early 50s therefore need to start planning ahead if they want to retire early, or intend to use some of their pension savings to clear debts like mortgages or meet other important expenses.

It's especially important to find out the age rules on your work and other personal pensions, because some people will continue to be able to access their funds at 55 depending on what they say.

Do your research: It is important to find out the age rules on your workplace or other private pension, and plan ahead if you want to retire early

'The over-55s are more likely to be in the dark than those aged between 18 and 34 about their retirement prospects,' says Helen Morrissey, head of retirement analysis at Hargreaves.

'This could be for a variety of reasons. Some could love what they do and have no plans to stop, others may have not yet really engaged.

'Others may have realised that right now, they don't have enough and are playing catch up so want to keep their options open.

'It might also be young people having confidence in when they want it to happen – before complexities have time to come up – like affordability!'

Hargreaves surveyed 1,600 people who are not retired, but are otherwise weighted to be representative of the UK adult population.

Separate research by Compare the Market found that retirement is the life milestone that people are delaying for the longest due to the cost of living, at 3.9 years on average.

Buying a first home came in second with an average delay of 2.5 years, according the poll of 2,000 people in Great Britain.

Meanwhile, an influential industry study looks at what individuals and couples need to save to have a minimum, moderate or comfortable retirement.

Couples need £22,400 for a basic lifestyle, £43,100 for a moderate standard of living and £59,000 for a more affluent retirement.

The Pension and Lifetime Savings Association study assumes you and a partner both qualify for a full state pension, which rose to £11,500 a year in April, but the figures do not include income tax, housing costs - if you rent or are still paying off a mortgage - or care fees.

Share this article

How to plan for retirement

Helen Morrissey of Hargreaves Lansdown offers the following tips, plus scroll down to find out what to do if you're worried you haven't saved enough to retire when you want.

1. Check in with your pensions and retirement planning from time to time

Having an idea of what you want from your retirement can give you an idea of how much it will cost and this in turn can give you a sense of how much you need to have saved.

Results of Hargreaves Lansdown poll of when people expect to retire

2. Use an online calculator (see the box above)

You can plug in your pension details, and it will tell you how much you are on track for and how much income that will generate for you in retirement.

You can even model the long-term impact of contributing more over time if you can afford the extra contributions.

3. Make sure you haven't lost track of old workplace pensions

This is easily done as we move around. That small pension that you had in a job 20 years back could well have grown to a sizeable sum and can make a major impact on how much you have.

It could even bring your retirement forward by a few years. Be sure to go through your paperwork and if you have lost track of a pension then contact the government's Pension Tracing Service to see if they can help you find it.

4. Consider consolidating your pensions

Having them all in one place gives a better idea of what you've got and improves retirement decision making. However, make sure you aren't incurring expensive exit fees by doing so.

You also need to make sure you aren't missing out on benefits such as guaranteed annuity rates which could boost your retirement income.

5. Check your state pension

This forms the foundation of people's retirement planning and there are very few people who are not reliant on it to some extent.

The fact that the most popular response given for when people will retire is between 66 and 70 is testament to this, given that state pension age is currently 66 and is on its way up.

How to sort out your pension if you fear it's falling short

1) If you are worried about whether you will have saved enough, investigate your existing pensions. Broadly speaking, you need to ask schemes the following questions.

- The current fund value.

- The current transfer value - because there might be a penalty to move.

- Whether the pension is in a final salary or defined contribution scheme. Defined contribution pensions take contributions from both employer and employee and invest them to provide a pot of money at retirement.

Unless you work in the public sector, they have now mostly replaced more generous gold-plated defined benefit - career average or final salary - pensions, which provide a guaranteed income after retirement until you die.

Planning retirement: A third of adults across all age groups anticipate stopping work between ages 66 and 70, and just 5 per cent expect to do so before they are 55

Defined contribution pensions are stingier and savers bear the investment risk, rather than employers.

- If there are any guarantees - for instance, a guaranteed annuity rate - and if you would lose them if you moved the fund.

- The pension projection at retirement age. You can use a pension calculator to see if you will have enough - these are widely available online.

2) You should add the forecast figures to what you anticipate getting in state pension, which is currently £221.20 a week or around £11,500 a year if you qualify for the full new rate. Get a state pension forecast here.

3) If you are tempted to merge your old pensions, read our guide first to ensure you won't be penalised.

4) If you have lost track of old pots, the Government's free pension tracing service is here. Our retirement columnist, Steve Webb, has a guide to finding lost pensions here.

Take care if you do an online search for the Pension Tracing Service as many companies using similar names will pop up in the results.

These will also offer to look for your pension, but try to charge or flog you other services, and could be fraudulent.