When will interest rates fall again? Forecasts on when base rate will be cut

The Bank of England is expected to hold interest rates at its next meeting, after inflation rose above its 2 per cent target.

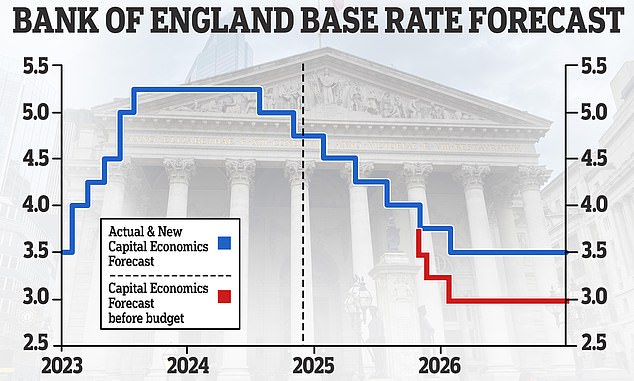

Earlier this month, the base rate was cut to 4.75 per cent from 5 per cent by a vote of 8 to 1 at the Monetary Policy Committee with the bank expecting base rate to end next year at about 3.7 per cent.

However, the ONS has now revealed that inflation rose to 2.3 per cent in the 12 months to September, above what markets were forecasting.

The surprisingly large rebound in inflation now has many predicting the central bank will leave interest rates at 4.75 per cent when it next convenes on 19 December.

The Bank of England cut interest rates at its November meeting, but inflation has now risen above its 2 per cent target

Latest on interest rates

The base rate was cut by the Bank of England at the November meeting after a hold last time round in September. That in turn followed August's cut from 5.25 per cent to 5 per cent.

It is thought that falling inflation played a major role in swaying the majority of Monetary Policy Committee members to vote in favour of a cut this month.

But now inflation in on the rise again, Rachel Reeves's tax and spend Budget has raised question marks over how far and fast rates will fall, and the Office of Budget responsibility forecasting a higher base rate than markets had expected.

Looking further ahead, UK and US headline interest rates are now forecast to reach 4 per cent by Christmas 2025 by market. This was 3.5 per cent only a couple of months ago.

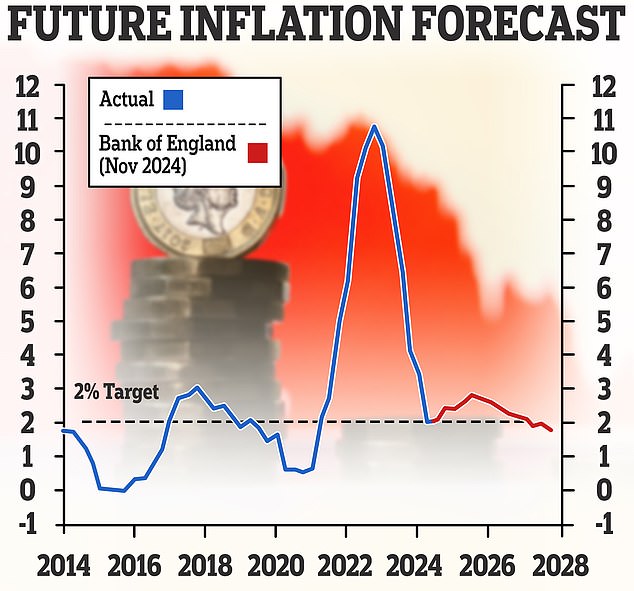

Inflation forecast: The Bank of England expects the rate of inflation to hover just above 2 per cent until 2027

As is to be be expected, forecasts vary.

The most bullish forecasters on rate cuts have base rate coming down to as low as 2.75 per cent by the end of 2025, with Goldman Sachs analysts announcing this rate forecast recently.

Goldman's prognosis would mean a quarter point interest rate cut at all nine meetings of the Bank's Monetary Policy Committee (MPC) from November 2024 to November 2025.

At the more reserved end of the spectrum, Santander recently revealed it expects interest rates to fall to 3.75 per cent by the end of next year.

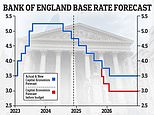

Meanwhile, economists at Capital Economics think the base rate will fall to 3.5 per cent by early 2026.

They had previously forecast that interest rates would fall to 3 per cent by the end of next year, but have concluded that rates will now fall slower as a result of the Labour's first budget.

New forecast: Capital Economics (CE) has changed its interest rate forecast because it now thinks the Bank of England will cut rates more slowly as a result of the budget

Paul Dales chief economist at Capital Economics said: 'We already thought that the Bank's inflation concerns would mean it continues to cut rates by 25basis points every quarter until mid-2025.

'But in the light of the Budget, we have revised up our own GDP and core inflation forecasts.

'And as a result, we no longer think the pace of rate cuts will quicken in the second half of 2025 and we now think rates will fall only as far as 3.5 per cent in early 2026 rather than to 3 per cent.'

Looking even further ahead than late 2025 and early 2026, economists vary on where they think interest rates will level off.

Santander, for example, thinks interest rates will remain between 3 per cent and 4 per cent for the foreseeable future.

Capital Economics is predicting that base rate will eventually level off at 3 per cent.

Oxford Economics is predicitng that base rate will eventually fall to 2 per cent in 2027 where it will broadly remain throughout 2028 and 2029.

The base rate and the Bank of England

The Bank of England moves what is officially known as bank rate but more commonly called base rate to try to control inflation.

The theory is that raising interest rates lifts the cost of borrowing for individuals and businesses and thus reduces demand for it, slowing the flow of new money into the economy and applying the brakes.

In contrast, cutting interest rates lowers the cost of mortgage rates and other borrowing and increases demand, pushing the accelerator on the economy.

Higher savings rates also make saving more attractive, while lower rates encourage spending over setting money aside.

The MPC sets interest rates to try to keep consumer prices inflation (CPI) at the Bank and Government's 2 per cent target.

> Interest rate rise and fall calculator: How moves affect your payments

Inflation spiked to 2.3 per cent in October as fears grow over the impact of the Budget and global trade tensions

What's happened to inflation and interest rates

A major inflation spike over recent years saw CPI rocket into double-digit territory, driven by the aftermath of the disruptive Covid lockdowns combined with an energy price crisis triggered by Russia's invasion of Ukraine.

This saw the Bank of England raise base rate rapidly from its record low of 0.1 per cent, reached during the Covid pandemic years.

The first move up to 0.25 per cent came in December 2021 and a sharp series of rises from the MPC followed, driving base rate all the way up to 5.25 per cent in August 2023.

Rates were then held at 5.25 per cent until August 2024, when they were cut to 5 per cent. The next cut was to 4.75 per cent in November 2024.

Stick or twist: The US Central bank recently cut rates

Watch the Fed on US interest rates

UK base rate moves have tended to follow a similar route as the Federal Reserve in the US and are also influenced by other major central banks.

It makes sense to be moving in a similar direction to other central banks, such as the Fed and the European Central Bank (ECB) to limit fluctuations in the pound, which can cause inflation to rise or fall..

Although the ECB cut rates to 3.75 per cent in June and then cut to 3.5 per cent for the eurozone in September, the US kept people waiting.

But a bumper 0.5 percentage point Fed rate cut arrived in September, along with doveish comments from Fed chair Jerome Powell on rates continuing to fall.

The fed followed this up in early November by reducing its policy rate by a further 0.25 percentgage points.

What next for interest rates?

For almost two years, the Bank of England attempted to combat rising inflation by continually upping the base rate.

Now the central bank is keeping a keen eye on disinflationary factors, such as any uptick in unemployment and stalling economic growth.

At present, markets are pricing in three interest rate cuts between now and the end of next year.

This could see the base rate will fall to 4 per cent by the end of 2025.

Second cut: The Bank of England has cut interest rates by 0.25 percentage points to 4.75% in November 2024

What base rate means for savings and mortgage rates?

Many people assume that savings rates and mortgage rates are directly linked to the Bank of England base rate.

In reality, future market expectations for interest rates and banks' funding and lending targets and appetite for business are what really matters.

Market interest rate expectations are reflected in swap rates. A swap is essentially an agreement in which two banks agree to exchange a stream of future fixed interest payments for another stream of variable ones, based on a set price.

These swap rates are influenced by long-term market projections for the Bank of England base rate, as well as the wider economy, internal bank targets and competitor pricing.

In aggregate, swap rates create something of a benchmark that can be looked to as a measure of where the market thinks interest rates will go.

Cause and effect: Inflation and wage growth are both factors that could determine what the Bank of England will do with base rate in the future

Current swap rates suggest that interest rates will be lower over the coming years, but not dramatically so.

As of 18 November, five-year swaps were at 3.99 per cent and two-year swaps at 4.22 per cent - both trending well below the current base rate.

Roughly this time last year, five-year swaps were around 4.5 per cent. Similarly, the two-year swaps were coming in above 5 per cent.

That said swaps have been edging upwards over the past month and this has caused some mortgage lenders to begin upping rates again.

Any borrowers hoping for a return to the rock bottom interest rates of 2021 will likely be disappointed. On the flipside, savers will be reassured that rates are not expected to plummet to the depths again.

It's worth pointing out that while swap rates are a good metric for where markets think interest rates are going, they also change rapidly in response to economic changes.

Richard Carter of Quilter Cheviot adds: 'Swap rates are a useful indicator of current expectations, but it is important to remember they are no better at predicting the future than any other economic indicator. The economic outlook can change very quickly and very dramatically.'

> Saving and banking: Read the latest on savings rates and top deals

What should savers do?

Experts foresee savings rates falling now that the Bank of England has cut the base rate.

Savers can still get close to 5 per cent in a standard easy-access savings account or easy-access cash Isa, and fixed rate savings offer similar deals at the moment.

Rachel Springall, finance expert at Moneyfacts said: 'Savers are the ones who feel the force of cuts to interest rates, and to add insult to injury, will see no rise to any personal tax or savings allowances in the short-term, making cash Isas increasingly attractive.

'Those savers who use their interest to supplement their income will feel overlooked if rates plummet.

'In December 2021, the average easy access rate stood at a pitiful 0.2 per cent and it took months for this to rise above a measly 1 per cent - even though the Bank of England base rate had risen from 0.1 per cent to 2.25 per cent over that time.

'Safe to say, it's understandable that savers feel hard done by, barely seeing a return on their money and in fact, watching the true value of their cash eroded by unprecedented high inflation.

'This could in turn, create an almost apathetic attitude among savers today, even as the average easy access account pays around 3 per cent, bank base rate is higher.

'Shockingly, there are UK current or savings accounts out there earning no interest whatsoever, £252bn worth in fact, according to the Bank of England.'

Check in: Keeping an eye on inflation is key to knowing whether or not your savings are being eaten away by inflation

The good news is that inflation now at 1.7 per cent it means savers who hold their cash in the top paying accounts will be making a decent real return, albeit before tax.

Our savings tables show the best easy-access savings, top cash Isas and fixed rate savings deals.

The advice to savers has been to keep on top of the changing market if they want to secure a competitive deal.

Springall adds: 'Challenger banks are offering attractive returns and it would be unwise to overlook them when they have the same protections in place as a high street bank.

'Savers need to proactively keep on top of the best rates and review their pots regularly to see if they are getting a raw deal.'

> Sign up to our savings alerts and be the first to find out about top deals

What next for mortgage rates?

Mortgage rates had been on a downward trajectory until recently. Between the start of July and early October, the cheapest available five-year fixed rate mortgage fell from 4.28 per cent to 3.68 per cent.

Meanwhile, the lowest two-year fix fell from 4.68 per cent to 3.84 per cent during that time.

Now, they are creeping back up again with the lowest five-year fix at 4.14 per cent and the lowest two-year fix at 4.21 per cent.

Mortgage borrowers on fixed term deals should look to where markets are forecasting the base rate to go in future and how this ties in with when their fixed rate ends.

But they should also be aware that mortgage rates can be volatile and a flurry of rises or cuts can soon be reversed.

Banks tend to pre-empt base rate moves. They change their fixed mortgage rates on the back of predictions about when base rate will fall or how high it will go, and how long inflation will remain high.

Banks and building societies general view on the housing market and economy also affect their appetite to lend, which feeds through into whether they want to cut or raise rates on offer to increase or dampen demand.

In reality, the first base rate cut served as more of a symbolic moment for mortgage holders, rather than one that will make any meaningful difference.

Peter Stimson, head of product at MPowered Mortgages said: 'Anyone who declared 'mission accomplished' in Britain's battle against inflation last month spoke too soon.

'The return of inflationary pressure means the Bank of England is likely to adopt a 'wait and see' approach on any further Base Rate reductions, not just in December, but in the immediate months following as well.

'While this was to a large extent expected, it doesn't offer any relief to mortgagelenders and is unlikely to allow them to reduce the interest rates they offer to newcustomers in the run up to Christmas.

'Looking ahead to 2025, the pace of Base Rate cuts is now likely to be 'slower andlower' than it was just a few than few weeks ago, and this is being reflected in a rising swaps market which has already forced many lenders to increase their mortgage interest rates over the past few weeks.'

Will borrowers benefit from future base rate cuts?

Future base rate cuts are already largely baked into fixed rate mortgage pricing and means most borrowers won't notice much difference when it comes to their mortgage rates - even with further base rate cuts down the line.

The bulk of outstanding residential mortgages are fixed rate and for the vast majority of these people, the base rate change won't have any immediate impact anyway until their fixed term ends.

Robert Gardner, chief economist at Nationwide, said: 'Investors expect bank rate to be lowered modestly in the years ahead, which, if correct, will help to bring down borrowing costs.

'However, the impact is likely to be fairly modest as the swap rates which underpin fixed-rate mortgage pricing already embody expectations that interest rates will decline in the years ahead.'

The mortgage borrowers who stand to benefit the most are those on tracker and variable rates.

Variable rate mortgages include 'discount' rates and also standard variable rates (SVRs). Monthly payments on all these types of loan can go up or down.

Tracker rates follow the Bank of England's base rate plus a set percentage, for example base rate plus 0.75 per cent. They often come without early repayment charges, allowing people to switch whenever they like without incurring a penalty.

Standard variable rates are lenders' default rates that people tend to move on to if their fixed or other deal period ends and they do not remortgage on to a new deal.

These can be changed by lenders at any time, and will usually rise and fall when the base rate does - but they can go up or down by more or less than the Bank of England's move.

According to Moneyfacts, the average SVR is just shy of 8 per cent, which is a lot higher than the average of 4.4 per cent in December 2021 when base rate was just 0.1 per cent - but it will vary from lender to lender.